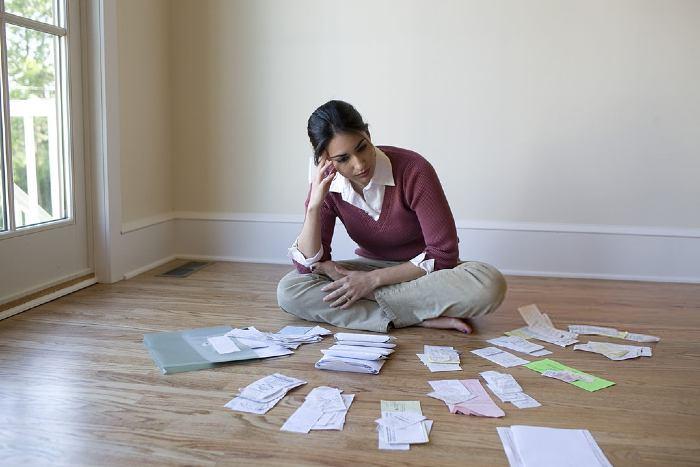

All of us make a budget with good intentions. Countless blogs are flooding the internet, explaining tips on how to make it and benefits. I never liked to make a budget. I found it a severe headache, killing my time. I started budgeting when it did not go very easy to manage cash for some considerable expenses. More often than not, I would be running out of money at the end of the month.

Credit card bills were due, and debt payments were outstanding by the time I started making a budget. Since online claiming, I was confident that this would help me be on top of my finances. For a couple of months, I continued to do it, but then I found it had a deleterious impact on my finances. Here are the reasons.

I set a goal, but I did not achieve it

My focus was not only cutting down on expenses and tracking spending. I could do it with my plain approach to handling money. I made a budget to build an emergency cushion and the other reason was borrowing on and off drove me crazy.

Four months fleeted by, but I was standing at the point from where I started. This flooded frustration in my veins. I thought tips I read were outlandish, far off the reality.

I consulted my friend, who was fond of budgeting. When he reviewed, he said the goal was unrealistic. While debt was lurking over my head, it wasn’t straightforward to manage to build the saving worth of three-month living expenses in just four months.

I was saving money when the debt was overdue

What to do first – pay down debt or save money – had always been a debatable topic. Some assume that it is wise to give priority to credit card bills over putting aside money as they carry very high-interest rates. They are, in fact, more expensive than short-term loans.

I took out bad credit loans to settle my credit card debt. Thankfully, I had to pay back a bad credit loan. Even though it came with a facility of instalment payments, it was getting on my nerves.

I skipped a payment on the due date, a disastrous move to fall into a debt cycle. I rigorously whittle down expenses to allow some room for saving as well as debt payment.

Despite experts’ recommendation not to save until debt settlement if it is very high, I continued to handle both simultaneously. I had blurred the boundaries between “what was controllable” and “what was uncontrollable”.

My financial condition became so worst that I had to apply for a CCJ loan with no guarantor with a direct lender. I was losing hope. Finally, I turned to a financial advisor. He recommended paying debt first.

I completely skipped the fun

Having fallen in debt, I made a restricted budget. I cut down on all discretionary expenses; even I stopped dining out. I left no room for fun because I had to build an emergency cushion while debt payment.

Before that terrible situation, I used to go out to entertain myself at the weekend. I stopped going anywhere. I was stuck in a rut, from home to work and then back home. This took a heavy toll on my health that I found myself in hospital, with a doctor sitting in front of me checking my nerves.

I was obsessed with tracking spending

People say they find budgeting annoying, but in my case, I was nagging at budgeting. I was so obsessed with implementing good financial habits that I started behaving idiosyncratically.

- I would consult my budget even before making a small purchase. I was overly protective of money.

- I panicked every moment I had to spend money.

- I spent nights awake evaluating how much I had spent throughout the day.

Message I learnt

The first thing I realised that budgeting could never be harmful when it comes to managing finances. Sometimes our approach does not let us take advantage of it. Besides, I learnt:

- Goals should be as realistic as possible.

- Debt should be paid off before setting aside money.

- Budgeting never expects us to skip fun altogether.

- Obsession can cause wreak havoc on our mental health.

This is my story. I hope you will not make the mistakes that I made.